Category: Free Video Tutorials

-

Stocks and Bonds Valuation in 60 minutes

For Stocks & Bonds Valuation EXAM TRAINING Click HERE (please donate)

-

Options: Put and Call Options Explained in 18 minutes

For Options Valuation and Black-Scholes click HERE (please donate)

-

Present Value and Future Value in 2 Easy Steps

CLICK HERE for Present Value Less than 1 Year, Present Value Compounding, Future Value Less Than 1 Year, Future Value Compounding. (Please donate).

-

Perpetuities and Annuities in 15 minutes

CLICK HERE for Present Value of Growing Annuity, Present Value of Annuity Due (or ‘Advanced Annuity’), Present Value of Delayed Annuity, Present Value of Growing Perpetuity (Please donate)

-

Payback Period – How to Calculate Payback Period in 6 min.

Introduction: Quick 3-Minute Overview

Part 1: Payback Period Calculation in 6 Minutes

Part 2: Payback Period In-Between Years

“Discounted” Payback Period Premium Video (Free Preview)

To Watch FULL Premium videos Click Here

-

NPV Net Present Value in 2 Easy Steps: What is NPV

Download my FREE Cheat Sheet on NPV at bottom of all videos below

3 Minute Overview: (Calculation at bottom)

10 Min. NPV Calculation & Explanation (super easy)

Net Present Value Exam Preparation (NPV Lease vs. Buy & NPV Investment 1 vs. Investment 2) – Premium Video (Free Preview)

To Watch FULL Premium videos Click Here

Download my FREE Cheat-Sheet PDF on NPV Net Present Value click here

CLICK HERE to get my premium videos which includes the NPV Exam Training Solution.

- NPV is similar to Present Value, but is more like different present values “combined.” Basically, it’s today’s value of different future values. (Huh??)

- Imagine you’re given different values in the future… and you use the present value formula on each of those future values; and then you combine it into just one present value. That’s your NPV!

- You calculate it using the NPV Net Present Value formula:

NPV = (Cash in or out today – if any) + (Cash in or out in Yr 1)-1 + (Cash in or out in next years)-n

- DON’T panic! It’s much EASIER than it looks. Watch it for free right now in the videos above.

Net Present Value is normally used to determine if a project is bad or good. If future cash flows have a NPV higher than a project’s cost, then the project is “good.” If it’s lower, then project is “bad”. Alternatively, if the project’s cost is already included in the NPV calculation, the project is “good” if the NPV is simply positive; and the project is “bad” if the NPV is simply negative.

-

IRR in 3 Easy Steps: Internal Rate of Return

See infographic and download FREE cheatsheet at bottom

3-Minute Overview

IRR Calculation Part 1

Part 2

Internal Rate of Return Exam Preparation – Premium Video (Free Preview)

To Watch FULL Premium videos Click Here

Download my FREE Cheat-Sheet PDF on Internal Rate of Return IRR click here

MAIN POINTS

- :

- Rate of return is “how fast” you can get back your money after you invest it. It’s expressed as a percentage per year, forever.

- For example, if you invest $100 and get back $3 per year (forever), then your rate of return is 3% (Because $3 = 3% of $100)

- Internal rate of return is the same as rate of return, except it’s not so easy to figure out like in the $3 example above. What if you get back $3 on the first year, but another amount in other years? And what if it’s not forever?

- In this case, we figure out this “mystery” rate of return (a.k.a. internal rate of return) using the IRR or Internal Rate of Return Formula:

0 = CF1(1+irr) + CF2(1+irr)-1 +…+ CFN(1+irr)-n

DON’T panic! It’s much EASIER than it looks. Watch tutorial video below.

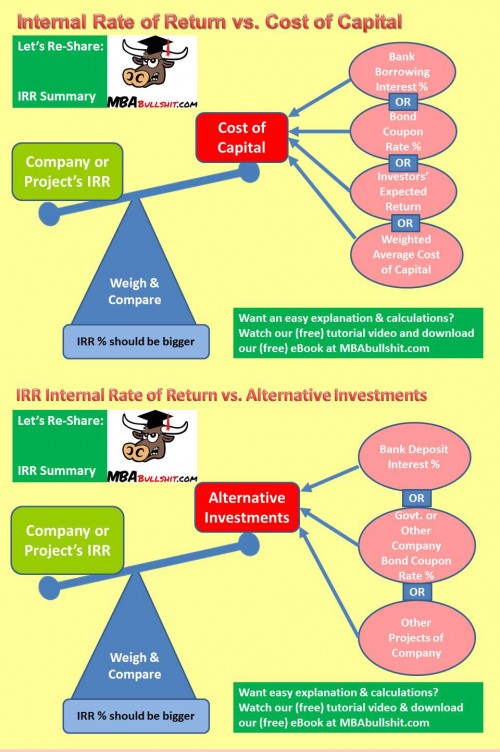

- IRR is used to gauge how “profitable” a business is, taking into account the amount invested in a company or a specific project

- IRR can be compared to cost of borrowing money for capital (or other sources of capital). For example: if your company’s capital comes from borrowing money from the bank at 5% interest rate, then your IRR should be higher than 5%… if your IRR is only 3%, then you are losing 2% (because 3% IRR less 5% bank interest will leave you with negative -2%)

- IRR can also be compared to your alternative investment choices. Why will you do a business project and earn only 3% IRR… if you can instead invest your money in a bank’s fixed term deposit which earns 4%? You are missing an opportunity to earn an extra 1%.